Property Week and lender Montello brought together some leading finance lights to discuss research on the future of property finance. Photographs by Paul Burroughs

Attendees:

- Giles Barrie, editor-in-chief, Property Week (chair)

- Christian Faes, managing director, Montello

- Adam Tyler, chief executive, National Association of Commercial Finance Brokers

- Daniel Schuldes, portfolio manager, Cheyne Capital

- Andrew Moffat, special projects, Pramerica

- Chris Philp, partner, Pluto Developments

Giles Barrie Let’s kick off with the state of the economy. Whether you believe the GDP figures or not, they’re not good.

Christian Faes It’s pretty dire — and not just the UK figures, but the eurozone and also the global economy. Now even China’s slowing down. But London is still a world unto itself.

Daniel Schuldes By now, we had hoped a stronger economic recovery would be coming out in the UK. It begs the question: has fiscal policy worked, or is a different combination needed?

GB Are there bargains lurking outside London?

Chris Philp Outside the capital, times are tough. Property markets, and businesses in general, are having to run hard to stand still. At a recent valuation of our residential portfolio in the south-east, prices were up by 7% over the past 18 months.In the north, where we manage a legacy portfolio, things are pretty bloody. The value of flats in Liverpool, for example, has fallen by a third but there’s still liquidity. You can sell them — at a price.

Adam Tyler To quantify how this has hit lending, in 2007, our members [who typically source commercial finance and bridging loans] were

writing £20bn of business between them. A year later, in 2008, that dropped 61% to just £6.5bn, but has now stabilised at about £10bn a year.

Our figures this year show a 108% increase in development finance, but that’s coming from a very small base, and is concentrated in the south-east. In 2010, we were struggling to find anyone who would lend outside London. I remember one of our members saying: “I don’t care if it’s a 1% loan-to-value in Barnsley, I’m not lending against it.”

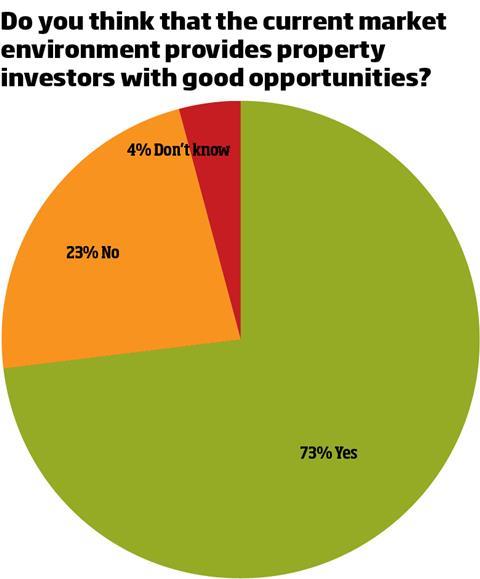

GB So where are the opportunities today?

Andrew Moffat If you’re investing with a five-year horizon, things look cheap. We’re already looking at secondary industrial assets, where there are equivalent yields on offer of more than 10%. Assuming you can relet some of the space, you can still make the numbers work without factoring in any growth. Assuming you could refinance at 75% in five years’ time, your return on equity could hit 20%. However, we are more nervous about high streets. You’ve got to be selective and know your towns. A lot of it will be killed off in the current cycle.

CP We expect to see 0% capital growth for the foreseeable future. Anyone who expects otherwise is endowed with a considerable amount of optimism. You’ve got to create something, and make an asset better. Our partner, Mountgrange, has recently picked up the £184m Mercury portfolio. There are huge opportunities to regear leases, relet space and create value without relying on the market going up.

GB Playing devil’s advocate, that’s assuming the tenants don’t go bust.

AT The fact is, local companies may well go bust, but it doesn’t mean they disappear. The phoenix will rise from the ashes, and the same local guys are still there, as there’s local demand. The worst type of tenants to go bust is the middle-ranking semi-national ones — when they go bust, they disappear.

GB How much will alternative lenders help?

AT There’s a lot of political pressure, and different government incentive schemes should help small businesses, who at long last will have money to invest in fulfilling new orders, employ staff and get the economy going. There is an alternative lending market outside the five high street banks but, even if these guys do what they’re saying they can, it’s never going to equal what the high street banks are doing. Funding Circle, the biggest peer-to-peer lender, gets a huge amount of PR, but I understand that they’ve only lent around £30m. It’s not about raising the money, it’s about deal flow.

GB Why should the government help banks lend to property investors?

CP Berkeley Homes chairman Tony Pidgley has argued that every £1 spent on development is equivalent to £3 in the wider economy because of the jobs it creates.

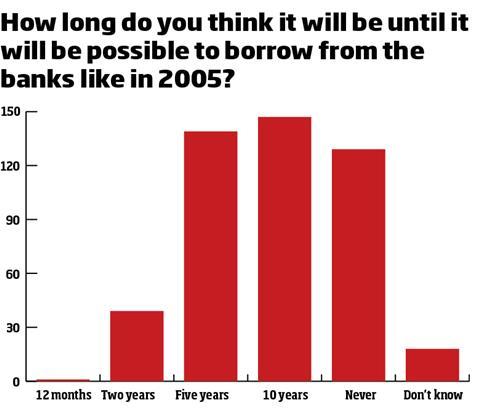

GB Will the heady bank lending levels of 2005 ever be seen again?

AM The big difference between now and the 1990s crash is that the capital rules meant banks were encouraged to make provisions, and there was an incentive to write everything down. Furthermore, interest rates were 10%, so problems had to be sorted out. Because of Basel II, the moment you make a bad loan, your balance sheet contracts. So it will be a far longer exit.

DS I agree — it will take at least 10 to 15 years.

AM Some way between 10 years and never is where I would fall.

GB What is the future for the banks?

CF If the banks don’t move back to those lending levels, other forms of funding will evolve. Our Montello Income Fund offers a fixed return to investors, and we lend it out against property. Investors invest in our conservative risk profile, our underwriting experience, and we don’t leverage our loan book, providing a superior risk-adjusted return for investors, and allows investors to capitalise on the market situation.

DS With our partner Omni, we’re providing bridging finance on residential projects between half a million pounds to £5m in value with a maximum loan to value of 80%. The problem for funders is it’s a relatively short-term market, you need to turn your book all the time and there’s a problem of scale. We’re looking for a similar type of investment with a longer maturity, and we find buy to let interesting.

GB Could the reduction in lending simply mean that people just don’t want to borrow money?

AT That’s a myth put about by high street banks.

CP Housebuilders want to build houses. I’m sure there’s appetite — there certainly is in our sector.

Research methodology

Four hundred and eighty Property Week readers took part in the survey in July 2012, via propertyweek.com

No comments yet