New lending has soared, banks’ exposure to distressed debt has plummeted and the number of active lenders in the market has increased, according to a survey.

The latest De Montfort property lending survey showed that as a result borrowers were benefiting from improved access to debt financing on increasingly favourable terms.

For loans secured on prime offices, average margins fell by 26.4bps to 226.5bps in the first six months of 2014, the report said. For secondary stock margins they fell even more, by 28.8bps to 275.7bps.

Initial market reaction to the findings has been upbeat. “There is a strong sense that the market has moved from dislocation to full recovery,” said Laxfield Capital director Emma Huepfl.

DTZ’s head of debt advisory Edward Daubeney added: “The report shows what a good diversification of lenders we now have in the market.

“We have lenders for prime London assets and lenders for more regional secondary assets.”

Non-bank lenders have cemented their position, with one joining the top 12 most active players for the first time, but the biggest change this year has been the rise of the US banks, who are willing to underwrite large loans and take mezzanine risk.

However, the 114-page report also exposed a continued lack of finance available for development and a significant disparity between the regions.

In towns such as Leeds, where there is now a shortage of good-quality office space available,

British Property Federation president Liz Peace said the current lack of debt finance was “concerning”.

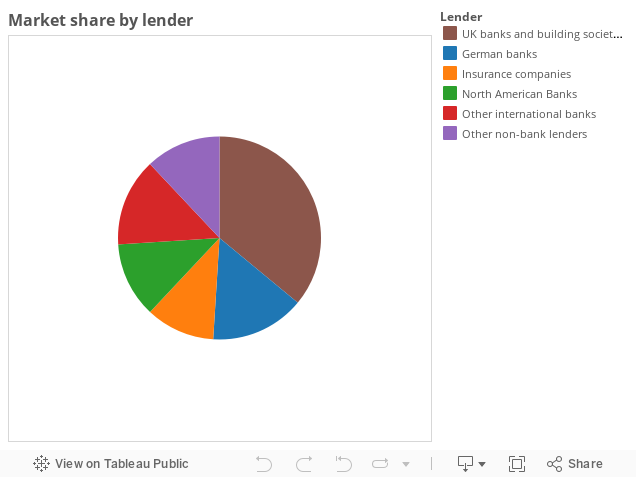

North American banks double market share

New lending in the first six months of 2014 hit £19.6bn - about two-thirds the £29.9bn lent during the whole of 2013. UK banks and building societies continued to be by far the most active lenders in the market, but their share of new lending slipped back from 43% last year to 36% in the first half of 2014.

Most other sub-groups saw little change in their market position, except North American banks, whose share rocketed from 5% to 12%. They lent £2.4bn in the first half of 2014, compared with £1.5bn during the whole of 2013. Non-bank lenders maintained the same 12% share as in 2013, but the survey revealed that one had joined its list of the 12 most active lenders.

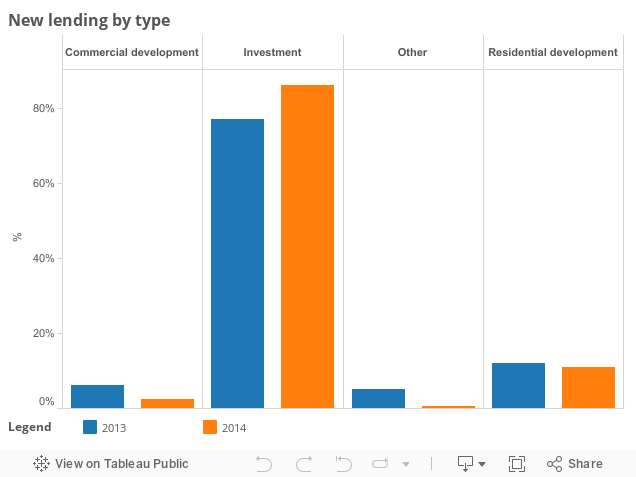

General reluctance to fund development

Lenders are still uneasy about development risk. Of those that said they were generally active in the wider property lending market, 55% said they would lend on fully prelet developments, 46% said they would lend on residential development for sale and 26% said they would lend on speculative developments.

On the plus side, more and more lenders are expressing a willingness to back development projects compared with 2013 when only 12% said they would fund speculative development.

However, this has yet to be reflected in any significant change in activity.

The portion of new lending from banks, building societies and insurance companies directed at development has fallen, particularly for commercial projects, which saw lending fall.

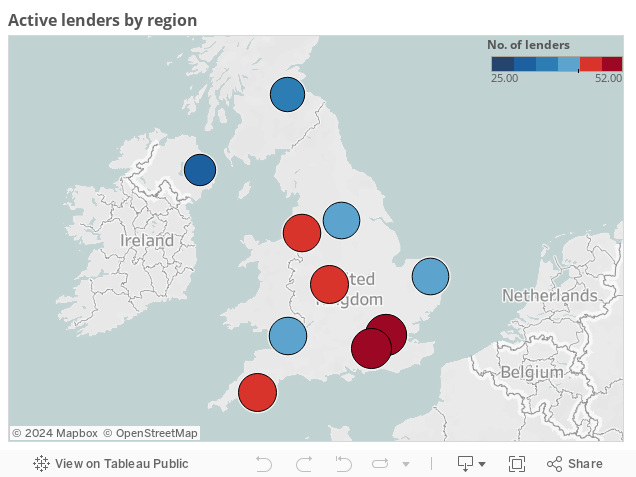

Lenders demonstrate strong London bias

For the first time, the De Montfort survey has tracked willingness to lend by region. It is no surprise that London tops the list, with 80% of lenders active in the market saying they would lend on prime investment projects in the capital.

At the opposite end of the spectrum, 55% said they would lend in Scotland and 46% said they were willing to lend in Northern Ireland. German and North American banks were prepared to lend in the regions, but other international banks had the strongest anti-regional bias of the different lenders. Whereas 11 international banks would fund London deals, on average half that would fund acquisitions outside

the capital.

For commercial development projects, lenders’ London bias was even more pronounced. Some 51% would be prepared to lend in London, versus as little as 14% in Northern Ireland.

No comments yet