A recent hospital visit with my ageing father provided me with first-hand experience of how a wider adoption of technology (eg. sharing of electronic medical records) could help to accelerate healthcare innovation.

Increasingly, operators will have to innovate to deliver an improved and more uniform quality of care or risk being taken over by stronger competitors. Such innovation will require financing and a better use of existing assets, which includes real estate.

The need for extra healthcare spending is not solely based on providing better care. Healthcare expenditure across France, Germany and the UK is already sizeable at about 10% of GDP. This is higher than transport, construction or education. During the past five years, healthcare spending has grown faster than either GDP or inflation.

Further increases are likely. First, long-term demographic trends point towards increased longevity: between now and 2030, there will be an additional 1.4 million people in the UK over the age of 80. Second, an increase in acute and chronic conditions will require additional spending. Third, healthcare consumption usually increases as nations become wealthier.

The taxpayer will find it more difficult to finance the extra expenditure. Currently, governments finance about 80% of healthcare spending in France, Germany and the UK. Except for Germany, most European governments are currently running a budget deficit - a situation which will only improve slowly given the moderate outlook for growth. The private sector, of which real estate is a part, will need to shoulder a larger share of healthcare financing. Our in-house research indicates the UK will have a healthcare funding gap of £34bn by 2020, a gap that the astute real estate investor can fill.

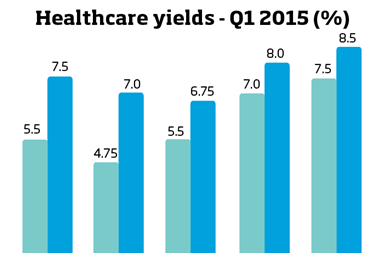

The European real estate healthcare sector is set to mature in a similar manner to that of the US. As at year-end 2014, US healthcare accounted for 11% of the overall REIT market capitalisation. In contrast, the UK healthcare market represents only 2.2% of the IPD UK Annual All Property Index.

In our view, the European market is likely to institutionalise further as a result The attraction to healthcare is performance driven: risk-adjusted returns from both the US and UK healthcare industries have outperformed that of mainstream real estate. For example, during the 2008 recession, US healthcare REIT prices suffered a peak-to-trough fall of 10%, while industrial and office REITs dropped 58%. A similar trend occurred in the UK, where healthcare performance suffered less than that of mainstream property.

Real estate healthcare investing is as much about the operator as the property. In a similar manner to hotels or data centres, real estate healthcare needs private equity underwriting expertise. The long-term demand drivers of the sector are supportive of real estate investments across the core value-add or development spectrum. For example, we are purchasing long income streams in the UK, Italy and Spain. Regulatory changes in Germany have resulted in a need to refurbish aged care homes, thereby providing value-add opportunities, and the private equity-led consolidation of operators in France and Germany provides a chance for investors to benefit from enhanced operating margins.

Ultimately, healthcare is likely to follow the path laid out by hotels. In the past 10 years, many hoteliers have moved towards an ‘asset light’ model. With the help of real estate investors, healthcare operators will be able to follow that trend and focus on delivering high-quality care.

Anne Kavanagh is global head of asset management and transactions at AXA Real Estate

No comments yet