Recommendations from the Barclay Review of Business Rates – including a £45m tax relief for new build properties – have been broadly welcomed by the Scottish property sector.

The year-long review into business rates in Scotland proposes that there should be a one-year relief from business rates for new build properties, which could be worth £45m to the economy. The tax incentive would also apply where there is a new tenant in place, supporting businesses that are relocating to new or redeveloped offices, shops or industrial premises.

Its author Kenneth Barclay, the former chair of RBS Scotland, also recommended that leisure centres, some golf clubs, private schools and universities should start paying into the system and that childcare centres should no longer pay the levy.

A three-year revaluation cycle is also proposed by the report, which suggests implementing a one-year gap between the date of market rental assessment and the revaluation coming into effect. Under the current system, the gap between rate reviews can be up to seven years.

Derek Mackay, Scotland’s finance secretary, welcomed the review and said the government would “respond swiftly” to its recommendations.

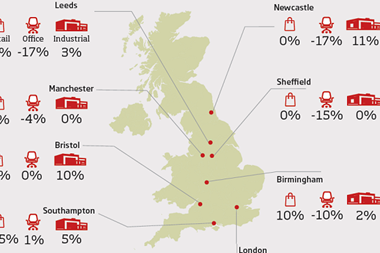

The 2017 revaluation, which took effect in April, has also prompted calls for reform to the system in England, where the UK government has said it aims to deliver more frequent revaluations at least every three years. Northern Ireland also plans to move to three-yearly revaluations from 2019.

Reactions

- Ken Thurtell, partner in Gerald Eve’s Glasgow office: ‘In reality, this review was never about addressing the 2017 Revaluation, despite many commentators expecting swift and radical change. What we have instead is a series of recommendations to implement minor short-term policy tweaks, with no prospect of major changes being delivered before Big Ben chimes next again in 2022. Despite some laudable recommendations, the review ultimately amounts to a congested road map full of potential delays and pitfalls and which remains very much at the discretion of a Government, which doesn’t have a great track record in accepting the recommendations of independent committees.”

- Niall Rankin, lead director for rating in Scotland at JLL: “The headline recommendation to adopt a three year rating cycle has been eagerly anticipated and has widespread support from the Scottish Assessors and ratepayers’ advisers. The current rating system in Scotland is notoriously unresponsive to change; appeals on the grounds of material change of circumstances are only granted in the most extreme circumstances. With this in mind, we fully welcome the recommendation to move to a three year cycle. The decision to use a multiplier based on CPI rather than RPI will make Scotland a more attractive place to do business and drive economic growth, by better reflecting the economic reality in the rates system.”

- Paul Curran, chairman of the Scottish Property Federation: “The Barclay proposals are hugely welcome and we encourage the Scottish Government to adopt them as soon as possible. We very much welcome the review’s recommendations to reduce Scottish large business supplement to the same level as its English equivalent in 2020/21 – therefore bringing about a level playing field across the UK and ensuring that the Scottish real estate market remains competitive with our neighbours south of the border.”

- John Webber, head of business rates at Colliers: “Some of the proposals relating to second homes, charities, listed buildings and agricultural land are quite radical. Some of these things will test the water. The Westminster government will be watching closely to see how these things are implemented and the reaction to it. The Westminster government might set themselves up as friends of agriculture, whereas Scotland could see them as an easy raid.”

- Huw Edgar, policy manager UK markets at RICS: “The proposal to introduce rates relief for extended or improved property may encourage expansion and business growth, while three-yearly revaluations would improve fairness and ensure rateable values are more reflective of market conditions. They would also negate the need for transitional relief.”

No comments yet